Bank Secrecy Act BSA Conference 2024: Get ready to dive deep into the ever-evolving world of financial crime prevention. This year’s conference promises actionable insights, cutting-edge strategies, and real-world case studies to help you navigate the complexities of BSA compliance. We’ll explore everything from the historical context of the Act to the latest technological advancements in combating financial crime.

The conference will cover crucial aspects of BSA compliance, including emerging trends, potential conflicts of interest among stakeholders, and the global perspective on BSA regulations. Expect a comprehensive look at innovative solutions for compliance, analysis of successes and failures, and a clear roadmap for future compliance efforts. Prepare to learn how to stay ahead of the curve and build a more secure financial system.

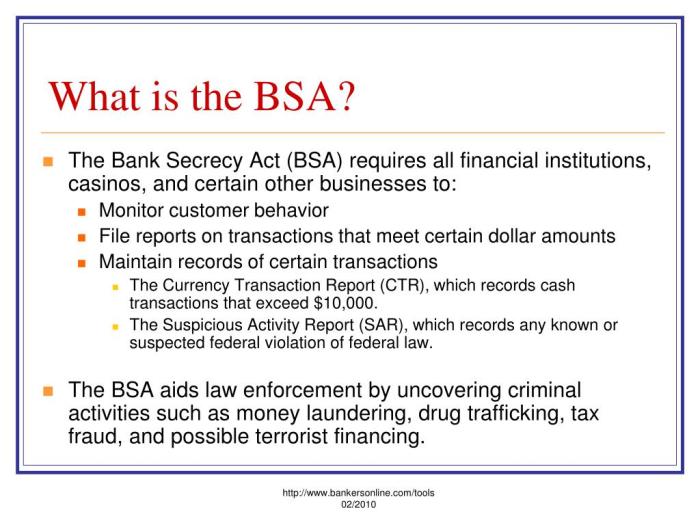

Background on the Bank Secrecy Act (BSA)

The Bank Secrecy Act (BSA) is a cornerstone of the US financial system’s fight against financial crime. It mandates that financial institutions collect and report certain information to the government, helping to detect and deter illicit activities. This legislation has evolved significantly over the years, adapting to changing threats and technological advancements. Understanding its history, objectives, and application is crucial for maintaining financial integrity.

Historical Overview of the BSA

The BSA was enacted in 1970, initially focusing on the reporting of currency transactions. Key amendments and updates over the years have broadened its scope and requirements. The USA PATRIOT Act of 2001 significantly expanded the BSA’s reach, adding provisions to combat terrorism financing and money laundering, particularly after the September 11th attacks. More recent updates reflect evolving financial technologies and international cooperation efforts, addressing issues such as virtual currencies and cross-border transactions.

These amendments underscore the BSA’s dynamic nature, continuously adapting to the evolving landscape of financial crime.

Primary Objectives and Goals of the BSA

The primary objectives of the BSA are to: detect, deter, and prevent financial crimes such as money laundering and terrorist financing. It aims to achieve this by requiring financial institutions to maintain records, file reports, and cooperate with law enforcement agencies. The BSA seeks to create a system where suspicious activities are flagged, investigated, and ultimately disrupted.

This holistic approach to financial crime prevention underscores the importance of vigilance and cooperation between financial institutions and regulatory bodies.

Role of the BSA in Combating Financial Crime, Bank secrecy act bsa conference 2024

The BSA plays a crucial role in combating financial crime by: establishing a framework for financial institutions to identify and report suspicious activity; creating a robust record-keeping system to track financial transactions; and fostering cooperation between financial institutions, law enforcement agencies, and regulatory bodies. These measures enhance the ability to trace illicit funds, identify perpetrators, and ultimately disrupt criminal networks.

The BSA’s effectiveness depends on the vigilance and commitment of financial institutions to comply with its requirements.

Types of Financial Institutions Covered by the BSA

The BSA applies to a broad range of financial institutions, including: banks, savings and loan associations, credit unions, money transmitters, casinos, and others engaged in financial transactions. This wide-ranging application ensures that the BSA covers various sectors of the financial industry, preventing illicit activities across the entire financial ecosystem.

Components of the BSA

The BSA encompasses several critical components, all crucial to its effectiveness in combating financial crime. These components work in tandem to create a comprehensive system for tracking and reporting suspicious activities.

| Component | Description |

|---|---|

| Currency Transaction Reporting (CTR) | Reporting of cash transactions exceeding a specified threshold, aimed at detecting the movement of large sums of cash that may be related to money laundering. |

| Suspicious Activity Reporting (SAR) | Reporting of suspicious activity, including transactions that raise red flags for money laundering or terrorist financing. This allows law enforcement to investigate potentially illicit transactions. |

| Recordkeeping Requirements | Maintaining detailed records of transactions, customer identification, and other relevant information for a specified period. This enables authorities to trace the origin and destination of funds. |

| Customer Identification Program (CIP) | Establishing procedures for verifying the identity of customers to prevent the use of accounts by individuals seeking to conceal their true identities. |

BSA Conference 2024 Focus Areas

The 2024 Bank Secrecy Act (BSA) conference promises to be a critical forum for discussing the evolving landscape of financial crime compliance. Attendees can expect in-depth analyses of emerging threats, innovative solutions, and the impact of recent legislation on financial institutions. This will facilitate a crucial exchange of best practices and strategies for navigating the complexities of BSA compliance in the modern financial environment.The conference will delve into the multifaceted challenges of maintaining robust BSA compliance in a constantly shifting regulatory environment.

Participants will explore the intricate interplay between evolving financial technologies, sophisticated criminal tactics, and the need for adaptive compliance frameworks. Key areas of focus will include the latest trends in financial crime, innovative solutions for risk mitigation, and the practical application of new legislation.

Potential Themes and Topics for Discussion

The conference will explore several crucial themes related to BSA compliance, including the intersection of technology and financial crime, the rise of cryptocurrencies and virtual assets, and the implications of international sanctions. Discussions will address the evolving nature of money laundering and terrorist financing schemes, encompassing emerging trends in illicit activity and the need for proactive, data-driven approaches to compliance.

The use of advanced analytics and machine learning in identifying suspicious activity will also be a prominent topic.

Emerging Trends and Challenges in BSA Compliance

The financial services industry faces evolving threats from sophisticated criminal networks exploiting technological advancements. The rise of cryptocurrencies and decentralized finance (DeFi) presents new challenges for financial institutions in identifying and mitigating risks associated with these emerging technologies. The increasing complexity of international transactions and the need for effective cross-border collaboration in compliance efforts will also be highlighted.

The challenge of maintaining compliance with ever-changing sanctions regimes is also a significant area of concern.

Innovative Solutions for BSA Compliance

Financial institutions are increasingly adopting innovative technologies to enhance their BSA compliance programs. These include advanced analytics platforms capable of identifying suspicious activity patterns, AI-powered tools for real-time transaction monitoring, and blockchain-based solutions for tracing assets and transactions. Furthermore, enhanced due diligence procedures, leveraging customer relationship management (CRM) systems and machine learning, can help mitigate risks. The adoption of open banking standards and the sharing of information between financial institutions will be explored as a means to enhance risk detection and reporting.

Recent Legislation Impacting the BSA

Recent legislative changes, such as the Anti-Money Laundering Act (AML) amendments, and the introduction of new regulatory guidelines for virtual assets, have significantly impacted the BSA compliance landscape. These legislative updates reflect the ongoing effort to adapt to the evolving nature of financial crime. The focus is on strengthening regulations to address emerging risks and enhancing the effectiveness of compliance frameworks.

Comparison of Compliance Strategies for Financial Institutions

| Compliance Strategy | Description | Strengths | Weaknesses |

|---|---|---|---|

| Proactive Monitoring | Employing advanced analytics and machine learning to identify potential risks in real-time. | Early detection of suspicious activity, reduced risk of financial crime. | High initial investment, requires specialized expertise. |

| Enhanced Due Diligence | Implementing stringent customer onboarding procedures and ongoing monitoring. | Improved risk assessment, compliance with KYC/AML requirements. | Increased operational costs, potential for compliance fatigue. |

| Collaboration and Information Sharing | Facilitating information exchange between financial institutions and law enforcement agencies. | Improved detection of cross-border financial crimes, enhanced risk mitigation. | Privacy concerns, data security challenges. |

“Effective BSA compliance requires a multifaceted approach, integrating technological advancements, robust due diligence processes, and strong partnerships within the financial ecosystem.”

Key Players and Stakeholders

The Bank Secrecy Act (BSA) compliance landscape is complex, involving numerous stakeholders with diverse roles and responsibilities. Understanding these relationships and potential conflicts is crucial for effective implementation and enforcement of BSA regulations. This section delves into the key players, their respective duties, and the potential tensions arising from differing perspectives on BSA compliance.

The 2024 Bank Secrecy Act (BSA) conference promises a profound exploration of financial transparency, a crucial element in the unfolding tapestry of global interconnectedness. Yet, even as we navigate the complexities of financial regulation, we must remember the ephemeral nature of material possessions and the importance of inner peace. This awareness is beautifully exemplified by the community support offered at Skinner Funeral Home Eaton Rapids , a testament to the enduring human connection that transcends the veil of worldly affairs.

Ultimately, the BSA conference, like all endeavors, serves as a reminder of our shared humanity and the profound interconnectedness of all things.

Major Players Involved in BSA Compliance

Various entities play critical roles in ensuring BSA compliance. These include regulators, financial institutions, law enforcement agencies, and, increasingly, industry self-regulatory organizations. Each stakeholder contributes unique expertise and resources to the overall framework.

- Regulators: Government agencies, such as the Financial Crimes Enforcement Network (FinCEN) in the United States, play a pivotal role in establishing and enforcing BSA regulations. They set standards, conduct examinations, and issue guidance to financial institutions, ensuring adherence to the law. Their primary responsibility is maintaining financial system integrity and preventing financial crime.

- Financial Institutions: Banks, credit unions, money transmitters, and other financial institutions are the primary targets of BSA regulations. They are obligated to implement and maintain robust compliance programs, including customer due diligence (CDD) measures, suspicious activity reporting (SAR) procedures, and record-keeping requirements. Their responsibility is to actively mitigate financial crime risks and report suspicious transactions.

- Law Enforcement Agencies: Agencies like the FBI, IRS, and state law enforcement agencies are vital in investigating suspicious activities reported by financial institutions or uncovered through other means. Their responsibility is to investigate potential violations of the BSA and related statutes and bring violators to justice. They work closely with regulators to identify and address financial crime trends.

- Industry Self-Regulatory Organizations: Professional associations and industry groups can play a supporting role in BSA compliance. They provide guidance, training, and best practices to their members, thereby promoting consistent and effective compliance across the financial sector. Their role is to foster industry best practices and standards in addition to the mandated regulations.

Potential Conflicts of Interest

Disparities in perspectives and objectives can create potential conflicts between stakeholders. Regulators may prioritize broader systemic risks, while financial institutions focus on operational efficiency and profitability. Law enforcement agencies may prioritize rapid responses to reported suspicious activity, potentially at the expense of a thorough investigation. These differing perspectives can lead to friction and challenges in maintaining a unified approach to BSA compliance.

Stakeholder Perspectives on BSA Compliance

Different stakeholders have varying perspectives on the complexities and implications of BSA compliance. Regulators may prioritize risk-based approaches to compliance, while financial institutions may emphasize the cost and operational burden of stringent regulations. Law enforcement agencies may be concerned about the timeliness and quality of reported suspicious activities.

Relationships Between Stakeholders

A well-functioning BSA framework requires strong collaboration and coordination between stakeholders. Effective communication channels and clear roles are essential to maintain the integrity of the system.

| Stakeholder | Regulators | Financial Institutions | Law Enforcement | Industry Self-Regulatory Organizations |

|---|---|---|---|---|

| Regulators | (Self-regulation) | (Setting standards, examinations, guidance) | (Coordination on investigations) | (Guidance and support) |

| Financial Institutions | (Adherence to regulations) | (Self-regulation) | (Reporting suspicious activity) | (Best practices and standards) |

| Law Enforcement | (Information sharing, investigations) | (Collaboration on investigations) | (Self-regulation) | (Information sharing) |

| Industry Self-Regulatory Organizations | (Input on regulations) | (Guidance and support) | (Collaboration on best practices) | (Self-regulation) |

Technological Advancements and BSA

Technological advancements are profoundly reshaping the financial landscape, presenting both opportunities and challenges for BSA compliance. The increasing digitization of financial transactions and the rise of new technologies like artificial intelligence and blockchain necessitate a dynamic approach to combating financial crime. This evolution demands a comprehensive understanding of how these advancements impact BSA compliance, enabling institutions to leverage technology for enhanced detection and prevention while mitigating associated risks.The integration of technology into BSA compliance is no longer a future prospect; it is a current necessity.

Institutions must adapt to maintain compliance and effectively combat financial crime in this evolving digital environment. This includes not only adopting new technologies but also establishing robust governance frameworks and training programs to ensure appropriate use and mitigate potential risks.

Impact of Technology on BSA Compliance

Technological advancements have significantly altered the financial landscape, making it both easier to conduct legitimate transactions and to facilitate illicit activities. This necessitates a corresponding evolution in BSA compliance strategies. The increased speed and volume of transactions, coupled with the anonymity afforded by digital platforms, have made traditional compliance methods less effective. Institutions must adapt to these changes to maintain compliance and mitigate the evolving risks.

The Bank Secrecy Act (BSA) Conference 2024 delves into the intricate web of financial transparency, illuminating the hidden currents that flow through the global economy. Unveiling the veiled truths, it explores the interconnectedness of wealth and its implications. This understanding, however, transcends mere financial transactions. It resonates with the deeper truth that our actions, like the rewards offered by bank rewards majora’s mask , are reflections of our inherent nature, ultimately shaping the very fabric of reality.

The conference, therefore, serves as a crucial compass, guiding us toward a more enlightened and equitable future, reminding us of the profound interconnectedness within the universe. Thus, the BSA Conference 2024 holds the key to unlocking the secrets of our collective prosperity.

AI and Machine Learning in Financial Crime Detection

Artificial intelligence (AI) and machine learning (ML) are revolutionizing financial crime detection. These technologies can analyze vast datasets of financial transactions in real-time, identifying patterns and anomalies indicative of suspicious activity. AI algorithms can learn from historical data to develop predictive models that identify potential financial crimes before they occur. Sophisticated algorithms can also discern subtle patterns and anomalies that human analysts might miss.

Examples of Technology Improving BSA Compliance

Numerous technologies are enhancing BSA compliance. Advanced transaction monitoring systems utilize AI and ML to identify suspicious activity, flagging potentially illicit transactions for further investigation. Blockchain technology, while presenting challenges, also offers opportunities for enhanced transaction transparency and auditability. Biometric authentication systems are enhancing the security of customer accounts and reducing the risk of fraud. Furthermore, cloud-based platforms offer scalability and efficiency in managing large volumes of BSA-related data.

Methods for Mitigating Technology Risks in BSA Compliance

Implementing robust risk mitigation strategies is crucial when integrating technology into BSA compliance. These strategies should encompass data security protocols, including encryption and access controls, to prevent unauthorized access and data breaches. Regular security assessments and penetration testing are essential to identify and address vulnerabilities. Regular employee training on the responsible use of technology and the latest compliance regulations is essential.

Effective incident response plans must be in place to handle potential security breaches or compliance violations promptly and effectively.

Table: Potential Benefits and Drawbacks of Technological Solutions

| Technological Solution | Potential Benefits | Potential Drawbacks |

|---|---|---|

| AI-powered transaction monitoring | Enhanced detection of suspicious activity, reduced false positives, increased efficiency | Potential for bias in algorithms, dependence on data quality, high initial investment |

| Blockchain technology | Enhanced transparency and auditability, reduced risk of fraud, increased security | Complexity in implementation and maintenance, potential scalability issues, regulatory uncertainties |

| Biometric authentication | Increased security, reduced fraud risk, enhanced customer experience | Cost of implementation, potential for privacy concerns, dependence on reliable biometric data |

| Cloud-based platforms | Scalability, efficiency, reduced infrastructure costs | Security concerns related to cloud storage, reliance on third-party providers, potential for data breaches |

Global Perspective on BSA

The Bank Secrecy Act (BSA) is a cornerstone of financial crime prevention globally, requiring financial institutions to report suspicious activity and maintain records of transactions. Understanding its implementation and enforcement across various countries is crucial for effective international cooperation and combating the ever-evolving landscape of financial crime. This presentation examines the global landscape of BSA compliance, highlighting similarities, differences, and challenges in different jurisdictions.The effectiveness of BSA compliance varies significantly across countries, influenced by factors such as economic development, regulatory frameworks, and political stability.

This variability necessitates a nuanced understanding of the global landscape, emphasizing the importance of international cooperation and shared best practices. A comparative analysis of BSA regulations across nations reveals areas of convergence and divergence, providing valuable insights into the challenges and opportunities for harmonizing global standards.

BSA Compliance Across Different Countries

The implementation of BSA regulations varies significantly across countries. Some countries have adopted comprehensive regulations and robust enforcement mechanisms, while others face challenges in adapting to the complexities of the global financial system. This disparity in implementation can create significant risks in combating cross-border financial crime. Factors such as economic development, legal frameworks, and cultural contexts influence the effectiveness of BSA compliance efforts.

Comparison of BSA Compliance in Different Jurisdictions

BSA compliance differs across jurisdictions in several key aspects. Regulatory frameworks vary in their scope, breadth, and specificity. For instance, some countries have more stringent reporting requirements for certain types of transactions, such as those involving politically exposed persons (PEPs). Enforcement mechanisms also vary, with some countries having dedicated financial intelligence units (FIUs) with greater resources and expertise.

The level of financial sophistication and the prevalence of financial crime also impact the implementation and enforcement of BSA compliance regulations.

Role of International Cooperation in Combating Financial Crime

International cooperation plays a critical role in combating financial crime. Effective information sharing between countries is essential to identify and track illicit financial flows. Joint investigations and mutual legal assistance agreements are vital for apprehending criminals and recovering assets. Harmonization of BSA standards and best practices facilitates a more coordinated global approach to combating financial crime. This shared approach ensures that efforts are not confined by national borders.

Challenges of International BSA Compliance

Several challenges hinder the consistent application of BSA regulations globally. Jurisdictional differences in legal frameworks, regulatory interpretations, and enforcement capacities pose significant obstacles. Ensuring data privacy and security in cross-border information sharing is also a critical concern. Cultural and linguistic barriers, along with differing levels of financial literacy, can further complicate compliance efforts. Developing common standards for classifying and reporting suspicious activities across jurisdictions remains a persistent challenge.

Table Comparing BSA Regulations Across Various Countries

| Country | Key Regulatory Body | Reporting Requirements | Enforcement Mechanisms | Financial Crime Prevalence |

|---|---|---|---|---|

| United States | FinCEN | Comprehensive, including Suspicious Activity Reports (SARs) | Dedicated FIU with significant resources | High |

| United Kingdom | FCA | Robust requirements for AML/CFT | Strong enforcement framework | Moderate |

| China | PBoC | Increasingly comprehensive, focused on combating money laundering | Growing enforcement capabilities | High |

| India | RBI | Evolving requirements, adapting to global standards | Developing enforcement capacity | Moderate |

| Brazil | Central Bank | Specific regulations for financial institutions | Dedicated FIU with ongoing development | Moderate |

This table provides a simplified comparison. Specific regulations and enforcement procedures vary significantly within each country.

Case Studies of BSA Compliance Successes and Failures

Effective BSA compliance is crucial for financial institutions to prevent money laundering and terrorist financing. Successful implementations safeguard institutions from substantial penalties and reputational damage, while failures can result in severe consequences, including hefty fines, criminal prosecution, and erosion of public trust. Understanding both successful and unsuccessful strategies provides valuable insights for navigating the complex landscape of BSA compliance.

Examples of Successful BSA Compliance Efforts

Implementing robust BSA compliance programs is a proactive approach to risk mitigation. Successful strategies demonstrate a comprehensive understanding of the regulatory framework and a commitment to ongoing training and monitoring. These initiatives involve the development of detailed policies and procedures, effective internal controls, and regular risk assessments.

- A leading bank established a dedicated compliance department staffed by highly trained professionals. They implemented a sophisticated transaction monitoring system, utilizing advanced analytical tools to identify suspicious activity. This proactive approach allowed the bank to flag potential money laundering attempts early, significantly reducing the risk of financial crime. Their diligent compliance efforts resulted in a strong track record of compliance and earned the institution a reputation for robust AML/BSA practices.

- Another financial institution implemented a comprehensive employee training program that covered all aspects of BSA compliance, including the identification of red flags, reporting procedures, and the consequences of non-compliance. This proactive approach fostered a culture of compliance, enabling employees to recognize and report suspicious activity effectively. Regular updates and refresher courses ensured that knowledge remained current and relevant.

Examples of BSA Compliance Failures

Cases of BSA compliance failures underscore the importance of vigilance and continuous improvement. These failures often stem from inadequate policies, insufficient training, or a lack of commitment to the BSA regulatory framework.

- A financial institution experienced a significant BSA compliance failure due to a lack of adequate transaction monitoring systems. The institution failed to implement robust procedures for identifying suspicious activity, resulting in missed red flags and subsequent money laundering activities. This negligence led to substantial fines and reputational damage. The failure highlighted the critical need for up-to-date, sophisticated transaction monitoring systems.

- A smaller bank suffered a BSA compliance failure because of insufficient employee training. Employees lacked the necessary knowledge to identify suspicious transactions and report them appropriately. This resulted in a significant lapse in oversight, allowing money laundering to occur undetected. The resulting consequences included financial penalties and a tarnished reputation. The case underscores the necessity of comprehensive training programs and ongoing compliance education.

Causes and Consequences of BSA Compliance Failures

Several factors contribute to BSA compliance failures. These include a lack of robust policies, inadequate training, insufficient oversight, and a lack of commitment to ongoing compliance. The consequences of these failures can range from substantial fines to criminal prosecution and significant reputational damage.

- Inadequate Policies: A key cause of failure is the absence or weakness of policies and procedures that clearly define expectations for compliance. This leads to confusion and inconsistencies in practice, ultimately increasing the risk of non-compliance.

- Insufficient Training: Insufficient training on the BSA and related regulations leaves employees ill-equipped to recognize and report suspicious activity. This lack of training directly impacts the institution’s ability to detect and prevent financial crime.

- Insufficient Oversight: A lack of adequate supervision and monitoring mechanisms makes it difficult to identify and address compliance gaps. This absence of oversight can enable the perpetration of financial crimes undetected for extended periods.

- Lack of Commitment: A failure to prioritize and commit to ongoing compliance efforts can lead to a decline in vigilance and a rise in the risk of non-compliance. This often manifests in insufficient resources allocated to BSA compliance and a lack of executive sponsorship for compliance initiatives.

Lessons Learned from Case Studies

The analysis of BSA compliance successes and failures provides crucial lessons for financial institutions. The importance of proactive compliance, robust policies, ongoing training, and strong oversight cannot be overstated.

- Proactive Compliance: Successful compliance programs are characterized by a proactive approach to risk management, rather than a reactive response to incidents. This approach involves establishing robust internal controls, conducting regular risk assessments, and adapting to evolving threats.

- Strong Policies and Procedures: Comprehensive and clearly defined policies and procedures serve as a roadmap for compliance. These documents should be regularly reviewed and updated to reflect changes in regulations and best practices.

- Ongoing Training: Regular training sessions and updates are essential to keep employees informed about the latest BSA regulations and best practices. This includes hands-on training, simulations, and interactive sessions to reinforce knowledge and skills.

- Strong Oversight and Monitoring: A robust oversight and monitoring system is crucial to identify compliance issues and take corrective actions. This includes regularly reviewing transactions, analyzing data, and conducting internal audits.

Summary Table of Key Takeaways

| Category | Successful Compliance | Failed Compliance |

|---|---|---|

| Policies & Procedures | Comprehensive, clearly defined, regularly reviewed and updated | Vague, outdated, inconsistently applied |

| Training | Comprehensive, ongoing, interactive | Insufficient, infrequent, lack of hands-on experience |

| Oversight | Robust, continuous monitoring, regular audits | Weak, infrequent reviews, inadequate supervision |

| Resources | Adequate resources allocated to compliance | Insufficient resources allocated to compliance |

| Consequences | Strong reputation, minimal penalties | Significant fines, criminal prosecution, reputational damage |

Future of BSA Compliance

The Bank Secrecy Act (BSA) compliance landscape is constantly evolving, driven by technological advancements, shifting financial crime trends, and evolving regulatory expectations. Navigating this dynamic environment requires a proactive approach, encompassing ongoing education, adaptation to regulatory changes, and a forward-thinking perspective on emerging threats.

Anticipated Future Trends in Financial Crime and Compliance

Financial crime is becoming increasingly sophisticated, leveraging new technologies and exploiting vulnerabilities in existing systems. The rise of cryptocurrencies and decentralized finance (DeFi) presents novel challenges, demanding vigilance in identifying and mitigating associated risks. Cybercrime continues to pose a significant threat, with sophisticated attacks targeting financial institutions and their customers. The growth of the global digital economy also increases the need for robust KYC/AML processes across international transactions.

Furthermore, the increasing use of artificial intelligence (AI) and machine learning (ML) in financial operations presents opportunities for both compliance and crime.

Impact of Regulatory Changes on Future Compliance Efforts

Regulatory bodies worldwide are continuously refining and tightening BSA regulations to address emerging risks. These changes often mandate new reporting requirements, enhanced due diligence procedures, and stricter penalties for non-compliance. Financial institutions must remain abreast of these evolving regulations and adjust their compliance strategies accordingly. For example, the implementation of stricter international sanctions regimes demands heightened scrutiny of cross-border transactions.

The focus on combating financial terrorism also influences compliance requirements.

Importance of Ongoing Education and Training

Maintaining a strong foundation in BSA compliance requires consistent professional development. Regular training programs should equip personnel with the knowledge and skills necessary to identify and report suspicious activities effectively. This includes understanding the latest regulatory updates, evolving financial crime trends, and the application of new technologies to compliance procedures. Training should also emphasize ethical considerations and the importance of reporting suspected violations.

Effective training programs will also address cultural awareness and diversity to avoid potential blind spots in risk assessment.

Methods for Staying Updated on BSA Compliance Requirements

Staying informed about BSA compliance requirements necessitates proactive measures. Subscribing to regulatory bulletins, attending industry conferences and workshops, and engaging with professional organizations are crucial. Continuous monitoring of regulatory websites and publications for updates, as well as participating in online learning platforms dedicated to compliance, will enhance understanding. Financial institutions should also consider employing compliance officers specializing in the latest technological advancements to monitor evolving financial crime techniques.

Potential Implications of Future Trends on BSA Compliance

| Future Trend | Potential Implications on BSA Compliance |

|---|---|

| Rise of Cryptocurrencies and DeFi | Increased complexity in transaction monitoring, enhanced need for KYC/AML procedures for crypto assets, potential for money laundering and terrorist financing through DeFi platforms. |

| Sophisticated Cybercrime | Increased need for robust cybersecurity measures, enhanced monitoring of transactions for suspicious patterns, potential for data breaches impacting compliance records. |

| Global Digital Economy | Expansion of international transactions, need for enhanced cross-border compliance mechanisms, potential for increased complexity in identifying and mitigating risks. |

| Regulatory Tightening | Increased reporting requirements, stricter due diligence standards, higher penalties for non-compliance, need for compliance officers with advanced knowledge and training. |

| AI/ML Integration | Opportunities for automated risk assessment and transaction monitoring, need for expertise in using AI/ML for compliance, potential for bias in AI algorithms requiring mitigation strategies. |

Closing Notes

The Bank Secrecy Act BSA Conference 2024 promises a dynamic discussion on the ever-changing landscape of financial crime prevention. Attendees will gain a comprehensive understanding of the Act’s history, objectives, and the latest trends in compliance. From technological advancements to global perspectives, the conference will provide a wealth of knowledge and practical strategies for navigating the complexities of BSA compliance.

Ultimately, the conference aims to equip participants with the tools they need to effectively combat financial crime and build a more secure financial system.

FAQ Corner: Bank Secrecy Act Bsa Conference 2024

What are the key objectives of the Bank Secrecy Act (BSA)?

The BSA’s primary objectives are to prevent and detect money laundering and terrorist financing. It aims to help financial institutions comply with reporting requirements and recordkeeping standards to maintain transparency.

What are some emerging trends in BSA compliance?

Emerging trends include the increasing use of technology, such as AI and machine learning, to detect and prevent financial crimes. International cooperation and regulatory changes are also major factors.

How can financial institutions stay updated on BSA compliance requirements?

Staying updated involves ongoing education and training, close monitoring of regulatory changes, and actively seeking out resources and insights from experts like the ones at this conference.

What are some common challenges faced by financial institutions in complying with BSA?

Common challenges include keeping up with evolving regulations, adapting to technological changes, and ensuring consistent compliance across different jurisdictions.